For business owners, timing a mortgage is rarely straightforward. It is not just about interest rates. It is about how lenders assess your income, your structure, and your future risk.

Right now, there is a window where rates are showing volatility with a general downward trend, while lenders remain relatively flexible. That combination does not always last.

Mortgage Rates Are Showing Volatility With a Downward Trend

Over the past few weeks, we have seen a competitive shift. While headlines focus on the Bank of England, the real story for business owners is the tightening of lender margins.

Many high street lenders are currently absorbing some market volatility to win business. This is creating a strategic window where rates are becoming more competitive, even though underlying swap rates remain unpredictable due to global pressures.

With the next Bank of England interest rate decision set for Thursday 30th April 2026, many lenders are adjusting their pricing now to stay ahead of the curve.

For borrowers, this can mean:

- Improved affordability in the short term

- Greater competition between lenders

- Opportunities to secure favorable deals

Importantly, applying now does not remove flexibility. If rates reduce further before completion, we can switch to a better deal with the same lender, subject to criteria.

Economic Uncertainty Could Impact Your Borrowing

While rates are becoming more competitive, the broader outlook remains uncertain.

We are already seeing:

- Rising cost of goods affecting margins

- Global tensions influencing financial markets

- Inflationary pressure building

What may still come:

- Energy cost increases later this year

- Further pressure on operating costs

For business owners, this directly affects affordability. Even a small reduction in profit can reduce borrowing capacity, depending on how a lender assesses your income.

Lender Flexibility Is Strong Right Now

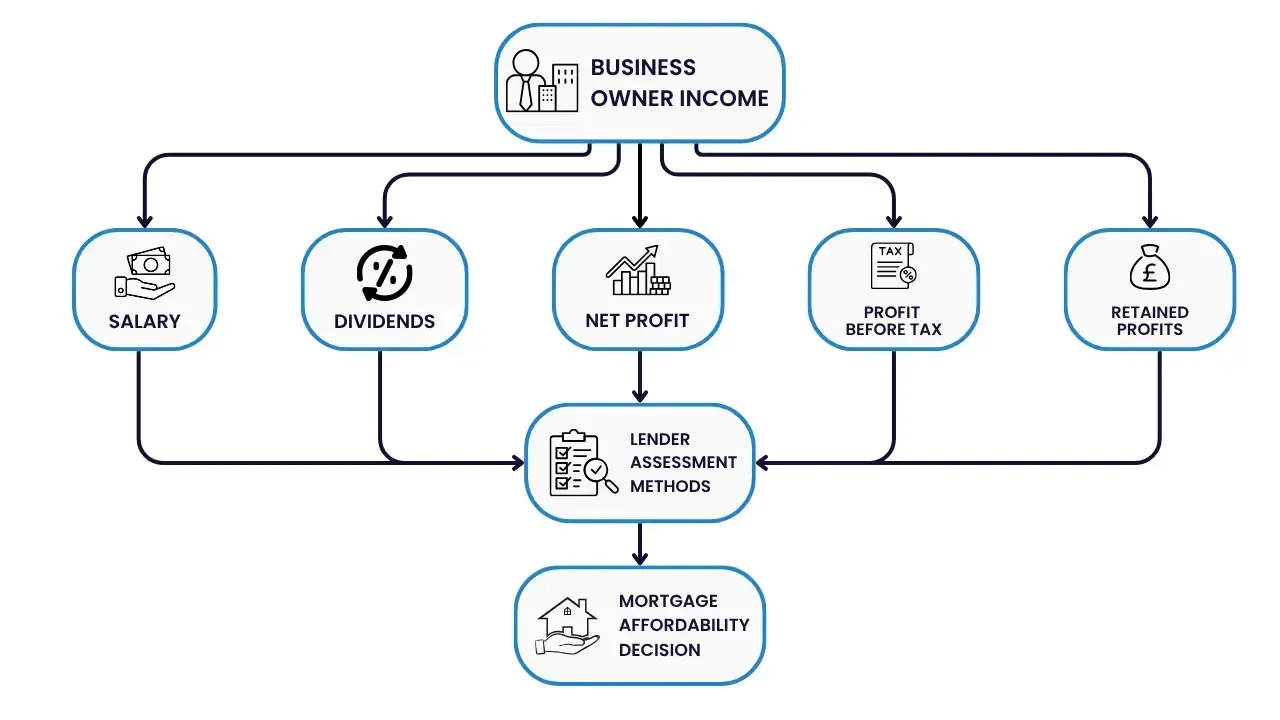

Currently, lenders are relatively open when assessing complex income structures. This is particularly relevant for directors, shareholders, and business owners with multiple income streams.

This includes:

- Using latest year figures or averaging two years

- Accepting salary and dividends combinations

- Utilising salary and share of profit after corporation tax

- Considering salary and profit before corporation tax in some cases

- Assessing more complex company structures

We are also seeing higher income multiples in some scenarios, with certain lenders willing to exceed traditional limits where affordability supports it.

This level of flexibility may change if market conditions shift.

Why Specialist Advice Matters More Than Ever

Many high street lenders rely on tick box underwriting and automated affordability models. These approaches do not always reflect the full financial position of business owners, particularly during periods of uncertainty.

This is where specialist advice becomes important.

Sarah Grace Mortgages focuses on understanding the full picture, including:

- Business performance over time

- Ownership structures

- Retained profits and sustainability

- Complex or multi-entity income

This approach can help identify lenders and solutions that may not be available through standard routes.

The Risk of Becoming a Mortgage Prisoner

Waiting for lower rates is a common strategy, but it carries a potential risk.

If you delay and your business experiences:

- A quieter trading period

- Increased costs

- Reduced profitability

You may find that even if rates improve, your borrowing options are more limited.

Securing a mortgage offer now can act as a form of protection. It allows you to access current criteria while retaining flexibility if the market improves, subject to lender terms.

History Shows Lending Can Tighten Quickly

When uncertainty increases, lenders often respond by tightening criteria.

We have seen this during:

- The 2008 financial crisis

- The COVID period

- Market instability in 2022

Typical changes include:

- Reduced income multiples

- Stricter affordability stress testing

- Less flexibility for complex cases

Business owners are often among the first to be affected.

Why Waiting Can Reduce Your Options

A wait and see approach may feel sensible, but it is not without risk.

If conditions change, you could face:

- Lower borrowing limits

- Reduced lender choice

- Increased scrutiny on your accounts

Applying now allows you to explore options based on current financials, lending criteria, and market conditions.

Example Scenario

A limited company director applies today using strong recent trading figures, including retained profits.

Today:

- A director with a £12,000 salary and £38,000 dividend and £80k in retained profit may qualify for a mortgage of around £460k

- Average of two years figures are used

- A higher income multiple may be available

Six months later:

- Costs increase and profits dip by 10 percent, or a lender no longer considers retained profits

Result:

- Borrowing capacity could reduce to around £250k

- Fewer lender options

- Stricter affordability assessment

This can happen even if interest rates are lower at that point.

TL;DR

- Mortgage rates are showing volatility with a general downward trend

- Lenders are currently competitive and relatively flexible

- Retained profits and complex income are still being considered

- Economic uncertainty may impact future affordability

- Applying now can help secure your current borrowing position

FAQs

Should I apply now or wait for rates to improve further?

Rates may improve, but lending criteria can also change. Applying now can provide flexibility while securing access to current options.

Can retained profits be used for a mortgage?

Yes, but it often requires a specialist lender. For many directors, your true income is what the business earns, not just what you pay yourself. By using retained profits, it may be possible to increase borrowing power without drawing additional dividends and creating unnecessary personal tax. Not all lenders accept this, so advice is important.

Can business owners still borrow large amounts?

In the right circumstances, it may be possible. Some lenders are currently offering higher income multiples where affordability supports it.

What income do lenders use for business owners?

This depends on the lender. It may include salary, dividends, net profit, or profit before tax

What happens if my business performance changes?

A reduction in profit may reduce borrowing capacity and lender choice. Each case will depend on individual circumstances and lender criteria.

[Contact Sarah Grace Mortgages Today]

Read more about: